I have spoken to more than a few pastors who mistakenly believe that mileage deductions went away after the Tax Cuts and Jobs Act. Before that misconception costs another dollar, read this.

The TCJA did change things for W-2 employees. Starting in 2018, workers can no longer deduct unreimbursed business expenses as miscellaneous itemized deductions on Schedule A. That part is true.

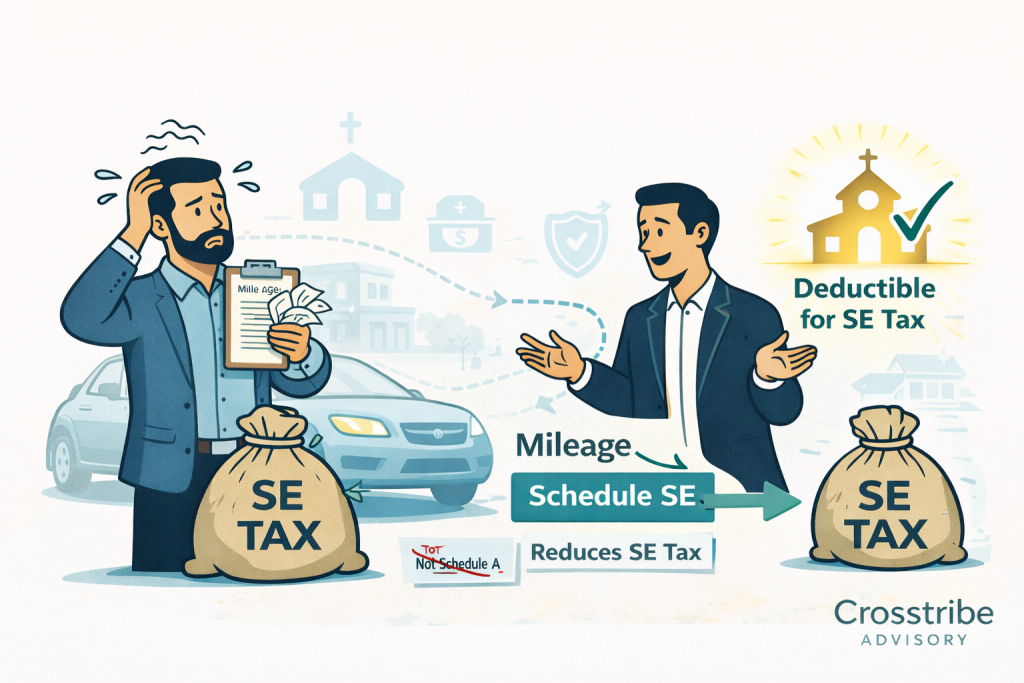

But clergy are not ordinary W-2 employees — and the mileage deduction did not disappear for them.

The IRS itself says it plainly. The current Instructions for Schedule SE state:

“If you were a duly ordained minister who was an employee of a church and you must pay SE tax, the unreimbursed business expenses that you incurred as a church employee are not deductible as an itemized deduction for income tax purposes. However, when figuring SE tax, subtract on line 2 the allowable expenses from your self-employment earnings and attach an explanation.”

— IRS Instructions for Schedule SE (Form 1040), 2025 edition

Read that again. Not deductible for income tax purposes — but subtract them when figuring SE tax. The IRS draws the line itself, in plain English, in a current document.

Here is what actually happened. After the TCJA passed, confusion spread — even among experienced tax professionals — because the law eliminated the Schedule A miscellaneous itemized deduction for unreimbursed employee expenses. The IRS even inadvertently removed the unreimbursed expense line from Worksheet 3 of Publication 517 in both the 2018 and 2019 editions. When tax professionals flagged the omission, the IRS issued a correction notice confirming it was a drafting error, not a policy change, and restored the line for the 2020 revision forward.

The deduction was never supposed to be removed. The Schedule SE instructions — which have carried this language consistently — confirm it.

Why does this matter for your pastor? Ministers are a special case under the tax code. They receive a W-2 for income tax purposes, but they are treated as self-employed for Social Security and Medicare tax purposes under SECA. That means their self-employment tax base — wages plus any housing allowance — can be reduced by ordinary and necessary ministry business expenses, including mileage.

Every hospital visit. Every shut-in call. Every home visit to a grieving family. Those miles are legitimate, documentable ministry expenses that reduce what your pastor owes in self-employment tax. At 72.5 cents per mile (the 2026 IRS standard mileage rate), those reductions add up fast.

The Schedule A issue and the Schedule SE issue are completely separate computations. The TCJA suspended miscellaneous itemized deductions under IRC §67(g) — that affects income tax on Schedule A only. Schedule SE operates under an entirely different statutory framework. The two computations run on separate tracks and always have. The Schedule SE instructions make this explicit.

✅ Unreimbursed mileage still reduces a minister’s SE tax base — the IRS Schedule SE instructions confirm this in the current 2025 edition.

✅ The IRS confirmed in writing that removing this line from Publication 517 was a drafting error.

✅ Schedule SE and Schedule A are independent computations governed by different code sections.

✅ Every undocumented ministry mile is real money your pastor is leaving on the table.

The best practice: set up an accountable reimbursement plan. Reimburse your pastor at the full IRS standard mileage rate with proper mileage log documentation — date, destination, business purpose. The reimbursement is tax-free to the pastor, deductible to the church, and eliminates the SE tax exposure entirely on those miles. No payroll tax. No SECA. Clean and simple.

If budget constraints make full reimbursement impractical, set an annual mileage budget and reimburse at the full IRS rate until the budget is exhausted. That approach is straightforward, defensible, and far better than an arbitrary per-mile cap or distance restriction that shifts real ministry costs onto your pastor’s personal finances.

Churches often do not see the full cost of ministry. When a pastor absorbs unreimbursed mileage with no tax relief, they are quietly subsidizing the church’s operations out of their own pocket. That is worth a conversation.

🙋 Not sure how your church’s current reimbursement setup stacks up?

Clergy tax law is one of the most misunderstood areas of the entire tax code — and the stakes are real. Crosstribe Advisory specializes exclusively in clergy and church taxation, helping ministry leaders stay compliant, protected, and free to focus on their calling.

👉 Book a free call at clergytaxadvisors.com

Don’t let a misread tax law cost your pastor money they don’t owe.

Sources: IRS Instructions for Schedule SE (Form 1040), 2025 edition | IRS Publication 517 (2025 ed.), Social Security and Other Information for Members of the Clergy and Religious Workers | IRS Correction Notice (2020), Pub. 517 Worksheet 3 | IRC §§ 1402(a), 1402(c), 67(g) | IRS Notice 2026-10 (2026 standard mileage rate)